Valuing Preferred Stock

For some reason, my paper on LendingTree and valuing preferred stock, which I had posted on this blog last year, seems to be getting a few hits... So I thought I would also post this follow up paper, which I had written a few years ago, in case any one finds it useful. A less mathematical, and much more useful explanation of liquidation preferences can be found in Feld Thoughts' term sheet series, here.

This paper outlines a methodology for valuing preferred stock and other complex financial instruments used primarily in ventre capital. Although venture capitalists appear to have a solid understanding of the capital structures they create, the analytical framework described here, as well as the graphical interpretations used to show the payout to stakeholders in a liquidation event, can serve in explaining some seemingly complex capital structures to management teams or stockholders who might have less sophisticated financial backgrounds.

Conversion to common stock

Standard terms for an investment in preferred stock would specify a conversion rate into common stock. If a company sells 10 million shares of preferred stock for $10 million at $1 per share, and each share of preferred stock is convertible into one share of common stock, and the company had 30 million common shares outstanding before the financing (with no debt), then the implied valuation of the firm after the financing (or the ‘post money value’) would be $40 million (assuming that the preferred stock had no other significant features). So,

Common Stock Equivalent Shares of the Preferred Stock,

CSES = # shares of preferred x conversion rate = 10 million

Common Stock Price,

CSP = Preferred stock price per share x conversion rate = $1

Common Stock Equivalent Ownership Percentage of the Preferred Stock,

CSEOP = CSES / (CSES + Number of common stock equivalent shares

outstanding before the transaction) = 25%

Post Money Value of the Company

PMV = CSES x CSP / CSEOP = $40 million

Liquidation preference The above framework provides the base case, which becomes more complex with the various provisions of the preferred stock. The liquidation preference is probably the most effective downside protection feature as it allows the investors in preferred stock to recover their investment (or a multiple of the investment) before the common stock receives any value. As the investors normally have seniority on this preference, and they may opt to treat the sale of the company as a ‘liquidation’ event, this preference is equivalent to the company taking on some debt. Liquidation preference is like a super-subordinated debt – the amount of preference is subordinated to all debt as well as to the creditors of the company, but senior to all equity in case of a liquidation of the company. (Note that for valuation purposes, one should value this debt by discounting the face value back from an assumed exit date, rather than at the face value of the liquidation preference.)

In the case above, a two times (2x) liquidation preference (and an immediate exit) would create $20 million of quasi-debt obligations that the company has to pay before the common stock is paid out. So each share of preferred stock would actually be equivalent to $2 of debt and one share of common stock. The post money value of the firm becomes:

PMV = LP + ( CSES x CSP / CSEOP )

where LP = Liquidation Preference

= Liquidation Pref. Multiple x Amount Invested = $20 million

But in this case, the Common Stock Price no longer has a direct relationship with the Preferred Stock Price (CSP Preferred Stock Price x conversion rate). Both PMV and CSP are unknowns in the above equation. In financing a company, a new investor would normally determine the post money value of the company using fundamental analysis and adjust the capital structure using the tools at his or her disposal. Or, if the capital structure is already in place, common stock holders can use the formula to determine the implied value of their holdings. For example, if we determine that the company’s PMV is $50 million, then the common stock is worth $0.75 per share, compared to the nominal value of the preferred stock of $1 per share. On the other hand, if a preferred stock investment has already been made in a publicly held company, we can use the traded value of the common stock to determine what the market believes to be the enterprise value of the firm.

In the above analysis, I have assumed that the preferred stock investors get what is called a ‘double dip’ liquidation preference, or a ‘participating preferred’ stock – that is, the investors receive both the liquidation preference as well as their common stock equivalent ownership share of the firm. But in many cases, investment terms dictate that the investors get the greater of their liquidation preference or their common stock equivalent ownership – a ‘simple preferred.’ For valuation purposes, this structure would imply that the investor receives the liquidation preference, but instead of getting straight common stock shares, in effect the investor acquires options on the common stock. That is, the investor will only receive compensation for the common stock equivalent ownership if the value of that stock is higher than the liquidation preference. Since the value of the investor’s common stock would be the ownership percentage (CSEOP) multiplied by the value of the firm, the company is in effect issuing options to the investor with a strike price equal to the liquidation preference divided by the common stock equivalent ownership. In the case above, still assuming a 2x liquidation preference, the strike price of the options would be at a firm value of $80 million ($20m / 25%.) In other words, each share of preferred stock would be the equivalent of $2 of debt and an option on common stock with a strike price of $2.

Note that it makes more sense to think about the preferred stock as debt plus common stock options from a new investor’s perspective. But if one is analyzing a publicly traded company , and the stock is trading above the conversion price of the preferred, it probably makes sense to think about the preferred stock as common stock plus a put on the common stock with a strike price equal to the conversion price of the preferred stock – which would be analytically equivalent to ‘debt plus common stock.’

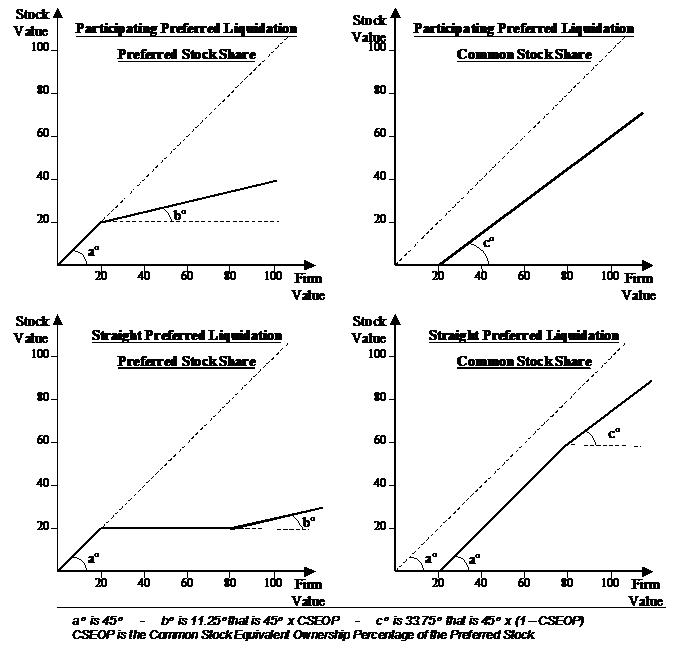

The chart below shows the difference between a simple and a participating preferred liquidation on the distribution of funds in case of a liquidation event. For companies with a number of classes of preferred stock, graphing out the remuneration to the different investors based on exit values can be illuminating to such investors and allows for clearer decision making. For example, one observation regarding the graphs is that the greater ownership stake an investor has in a company, the greater is the angle b and thus the less effective are the preferred stock’s downside protection features.

Options and warrants

From a practical point of view, it is important to have a method for valuing options within the framework laid out above. The easiest method for doing this is to value each option in common stock equivalent terms, so that each option is viewed as the equivalent of a portion of one share. As seen above, this portion can be calculated using reasonable assumptions in a simple Black-Scholes framework. As a result, we would have to recalculate the CSES.

In the example of the participating liquidation preference above, we noted that each share of preferred must be treated as $2 of debt plus one option for common stock at a strike price of $2 per share. If the common stock share price is $0.92 and we assume that the options have a 10-year expiration, volatility is 30%, and the simple interest rate is 5%, Black-Scholes tells us that each option would be worth $0.25, or 27.5% of the common stock value of $0.92. So,

Common Stock Equivalent Shares of the Preferred Stock,

CSES = # shares of preferred x Value of each option/CSP = 2.75 million

Then, although the formulas for CSEOP and PMV remain the same, their values change because of the recalculated value for CSES:

Common Stock Equivalent Ownership Percentage of the Preferred Stock,

CSEOP = CSES / (CSES + Number of common stock equivalent shares

outstanding before the transaction) = 8.4%

PMV = LP + ( CSES x CSP / CSEOP ) = $50 million

To illustrate the relationship between the different variables, we assumed a common stock price of $0.92 and reached the same PMV of $50 million. In practice, we would need to solve for the common stock price using the above formulas and our assumption for PMV, the fundamental value of the firm. Also, remember that in the case of the participating preferred stock, the same PMV of $50 million implied a common stock share price of $0.75.

This same methodology can be used for incorporating all of a company’s outstanding warrants and options in a total common stock equivalent capitalization table for the company. One interesting case is the value of warrants for preferred stock. In the above example, where the preferred stock has a 2x liquidation preference, each warrant for preferred stock would be worth $1 of liquidation preference (i.e., debt) plus one share of common stock. So warrants on preferred stock are more like debt and common stock, not warrants on common stock.

Dividends

Most preferred stock provides for some kind of dividend distribution. At first glance, it could be argued that mandatory dividends should be treated like the interest on debt and thus ignored in a valuation exercise. But this would only be the case if we value the preferred stock separately from the common stock of a company. By converting preferred stock into common stock equivalents, we reduce the number of unknowns from three (debt, common equity, and preferred stock) to two (debt and equity.) So the most reasonable approach to valuing the dividends in terms of common stock is to calculate the amount of dividends outstanding at the time of a potential exit and to include them in the number of common stock equivalent shares outstanding. So the inclusion of dividends depends on the method one uses to calculate the value of the company. If valued today, only accrued dividends would be counted – if fundamental analysis is used with an exit in three years, then three years of dividends should be calculated. And of course, this same logic would also apply to any liquidation preference that comes with those dividends.

Sometimes, investors agree to cancel their rights to dividends if the company achieves an exit that is above a certain valuation. In such a case, the value of the same dividend shares have to be calculated, but each potential dividend share should be treated as a put option on the value of the stock at the specified valuation.

Anti-dilution protection and ratchets

Most private financings have some sort of anti-dilution rights – the right for the investment to be re-priced at the next round of financing if that price is lower. Although this is a valuable right, there is no easy way to quantify it bar using Monte Carlo simulations or probability trees. One could also treat anti-dilution rights like out-of-the-money puts. But in practice, for new investors, these puts should be out of the money and of little value, unless there is a high probability of such dilution taking place.

Preferred Stock in Venture Capital A Valuation Methodology

This paper outlines a methodology for valuing preferred stock and other complex financial instruments used primarily in ventre capital. Although venture capitalists appear to have a solid understanding of the capital structures they create, the analytical framework described here, as well as the graphical interpretations used to show the payout to stakeholders in a liquidation event, can serve in explaining some seemingly complex capital structures to management teams or stockholders who might have less sophisticated financial backgrounds.

Conversion to common stock

Standard terms for an investment in preferred stock would specify a conversion rate into common stock. If a company sells 10 million shares of preferred stock for $10 million at $1 per share, and each share of preferred stock is convertible into one share of common stock, and the company had 30 million common shares outstanding before the financing (with no debt), then the implied valuation of the firm after the financing (or the ‘post money value’) would be $40 million (assuming that the preferred stock had no other significant features). So,

Common Stock Equivalent Shares of the Preferred Stock,

CSES = # shares of preferred x conversion rate = 10 million

Common Stock Price,

CSP = Preferred stock price per share x conversion rate = $1

Common Stock Equivalent Ownership Percentage of the Preferred Stock,

CSEOP = CSES / (CSES + Number of common stock equivalent shares

outstanding before the transaction) = 25%

Post Money Value of the Company

PMV = CSES x CSP / CSEOP = $40 million

Liquidation preference The above framework provides the base case, which becomes more complex with the various provisions of the preferred stock. The liquidation preference is probably the most effective downside protection feature as it allows the investors in preferred stock to recover their investment (or a multiple of the investment) before the common stock receives any value. As the investors normally have seniority on this preference, and they may opt to treat the sale of the company as a ‘liquidation’ event, this preference is equivalent to the company taking on some debt. Liquidation preference is like a super-subordinated debt – the amount of preference is subordinated to all debt as well as to the creditors of the company, but senior to all equity in case of a liquidation of the company. (Note that for valuation purposes, one should value this debt by discounting the face value back from an assumed exit date, rather than at the face value of the liquidation preference.)

In the case above, a two times (2x) liquidation preference (and an immediate exit) would create $20 million of quasi-debt obligations that the company has to pay before the common stock is paid out. So each share of preferred stock would actually be equivalent to $2 of debt and one share of common stock. The post money value of the firm becomes:

PMV = LP + ( CSES x CSP / CSEOP )

where LP = Liquidation Preference

= Liquidation Pref. Multiple x Amount Invested = $20 million

But in this case, the Common Stock Price no longer has a direct relationship with the Preferred Stock Price (CSP Preferred Stock Price x conversion rate). Both PMV and CSP are unknowns in the above equation. In financing a company, a new investor would normally determine the post money value of the company using fundamental analysis and adjust the capital structure using the tools at his or her disposal. Or, if the capital structure is already in place, common stock holders can use the formula to determine the implied value of their holdings. For example, if we determine that the company’s PMV is $50 million, then the common stock is worth $0.75 per share, compared to the nominal value of the preferred stock of $1 per share. On the other hand, if a preferred stock investment has already been made in a publicly held company, we can use the traded value of the common stock to determine what the market believes to be the enterprise value of the firm.

In the above analysis, I have assumed that the preferred stock investors get what is called a ‘double dip’ liquidation preference, or a ‘participating preferred’ stock – that is, the investors receive both the liquidation preference as well as their common stock equivalent ownership share of the firm. But in many cases, investment terms dictate that the investors get the greater of their liquidation preference or their common stock equivalent ownership – a ‘simple preferred.’ For valuation purposes, this structure would imply that the investor receives the liquidation preference, but instead of getting straight common stock shares, in effect the investor acquires options on the common stock. That is, the investor will only receive compensation for the common stock equivalent ownership if the value of that stock is higher than the liquidation preference. Since the value of the investor’s common stock would be the ownership percentage (CSEOP) multiplied by the value of the firm, the company is in effect issuing options to the investor with a strike price equal to the liquidation preference divided by the common stock equivalent ownership. In the case above, still assuming a 2x liquidation preference, the strike price of the options would be at a firm value of $80 million ($20m / 25%.) In other words, each share of preferred stock would be the equivalent of $2 of debt and an option on common stock with a strike price of $2.

Note that it makes more sense to think about the preferred stock as debt plus common stock options from a new investor’s perspective. But if one is analyzing a publicly traded company , and the stock is trading above the conversion price of the preferred, it probably makes sense to think about the preferred stock as common stock plus a put on the common stock with a strike price equal to the conversion price of the preferred stock – which would be analytically equivalent to ‘debt plus common stock.’

The chart below shows the difference between a simple and a participating preferred liquidation on the distribution of funds in case of a liquidation event. For companies with a number of classes of preferred stock, graphing out the remuneration to the different investors based on exit values can be illuminating to such investors and allows for clearer decision making. For example, one observation regarding the graphs is that the greater ownership stake an investor has in a company, the greater is the angle b and thus the less effective are the preferred stock’s downside protection features.

Options and warrants

From a practical point of view, it is important to have a method for valuing options within the framework laid out above. The easiest method for doing this is to value each option in common stock equivalent terms, so that each option is viewed as the equivalent of a portion of one share. As seen above, this portion can be calculated using reasonable assumptions in a simple Black-Scholes framework. As a result, we would have to recalculate the CSES.

In the example of the participating liquidation preference above, we noted that each share of preferred must be treated as $2 of debt plus one option for common stock at a strike price of $2 per share. If the common stock share price is $0.92 and we assume that the options have a 10-year expiration, volatility is 30%, and the simple interest rate is 5%, Black-Scholes tells us that each option would be worth $0.25, or 27.5% of the common stock value of $0.92. So,

Common Stock Equivalent Shares of the Preferred Stock,

CSES = # shares of preferred x Value of each option/CSP = 2.75 million

Then, although the formulas for CSEOP and PMV remain the same, their values change because of the recalculated value for CSES:

Common Stock Equivalent Ownership Percentage of the Preferred Stock,

CSEOP = CSES / (CSES + Number of common stock equivalent shares

outstanding before the transaction) = 8.4%

PMV = LP + ( CSES x CSP / CSEOP ) = $50 million

To illustrate the relationship between the different variables, we assumed a common stock price of $0.92 and reached the same PMV of $50 million. In practice, we would need to solve for the common stock price using the above formulas and our assumption for PMV, the fundamental value of the firm. Also, remember that in the case of the participating preferred stock, the same PMV of $50 million implied a common stock share price of $0.75.

This same methodology can be used for incorporating all of a company’s outstanding warrants and options in a total common stock equivalent capitalization table for the company. One interesting case is the value of warrants for preferred stock. In the above example, where the preferred stock has a 2x liquidation preference, each warrant for preferred stock would be worth $1 of liquidation preference (i.e., debt) plus one share of common stock. So warrants on preferred stock are more like debt and common stock, not warrants on common stock.

Dividends

Most preferred stock provides for some kind of dividend distribution. At first glance, it could be argued that mandatory dividends should be treated like the interest on debt and thus ignored in a valuation exercise. But this would only be the case if we value the preferred stock separately from the common stock of a company. By converting preferred stock into common stock equivalents, we reduce the number of unknowns from three (debt, common equity, and preferred stock) to two (debt and equity.) So the most reasonable approach to valuing the dividends in terms of common stock is to calculate the amount of dividends outstanding at the time of a potential exit and to include them in the number of common stock equivalent shares outstanding. So the inclusion of dividends depends on the method one uses to calculate the value of the company. If valued today, only accrued dividends would be counted – if fundamental analysis is used with an exit in three years, then three years of dividends should be calculated. And of course, this same logic would also apply to any liquidation preference that comes with those dividends.

Sometimes, investors agree to cancel their rights to dividends if the company achieves an exit that is above a certain valuation. In such a case, the value of the same dividend shares have to be calculated, but each potential dividend share should be treated as a put option on the value of the stock at the specified valuation.

Anti-dilution protection and ratchets

Most private financings have some sort of anti-dilution rights – the right for the investment to be re-priced at the next round of financing if that price is lower. Although this is a valuable right, there is no easy way to quantify it bar using Monte Carlo simulations or probability trees. One could also treat anti-dilution rights like out-of-the-money puts. But in practice, for new investors, these puts should be out of the money and of little value, unless there is a high probability of such dilution taking place.

posted by Salman FF at Sunday, November 20, 2005

4 comments

![]()